The Federal Reserve's First Rate Cut Since 2020: What It Means for You

In a significant move on September 18, 2024, the Federal Reserve reduced the federal funds rate by half a point, marking the first rate cut since 2020. This decision comes after a series of 11 rate hikes aimed at controlling inflation, which had been a pressing issue since 2022. So, what does this mean for the economy, mortgage rates, and your investments? Let’s break it down:

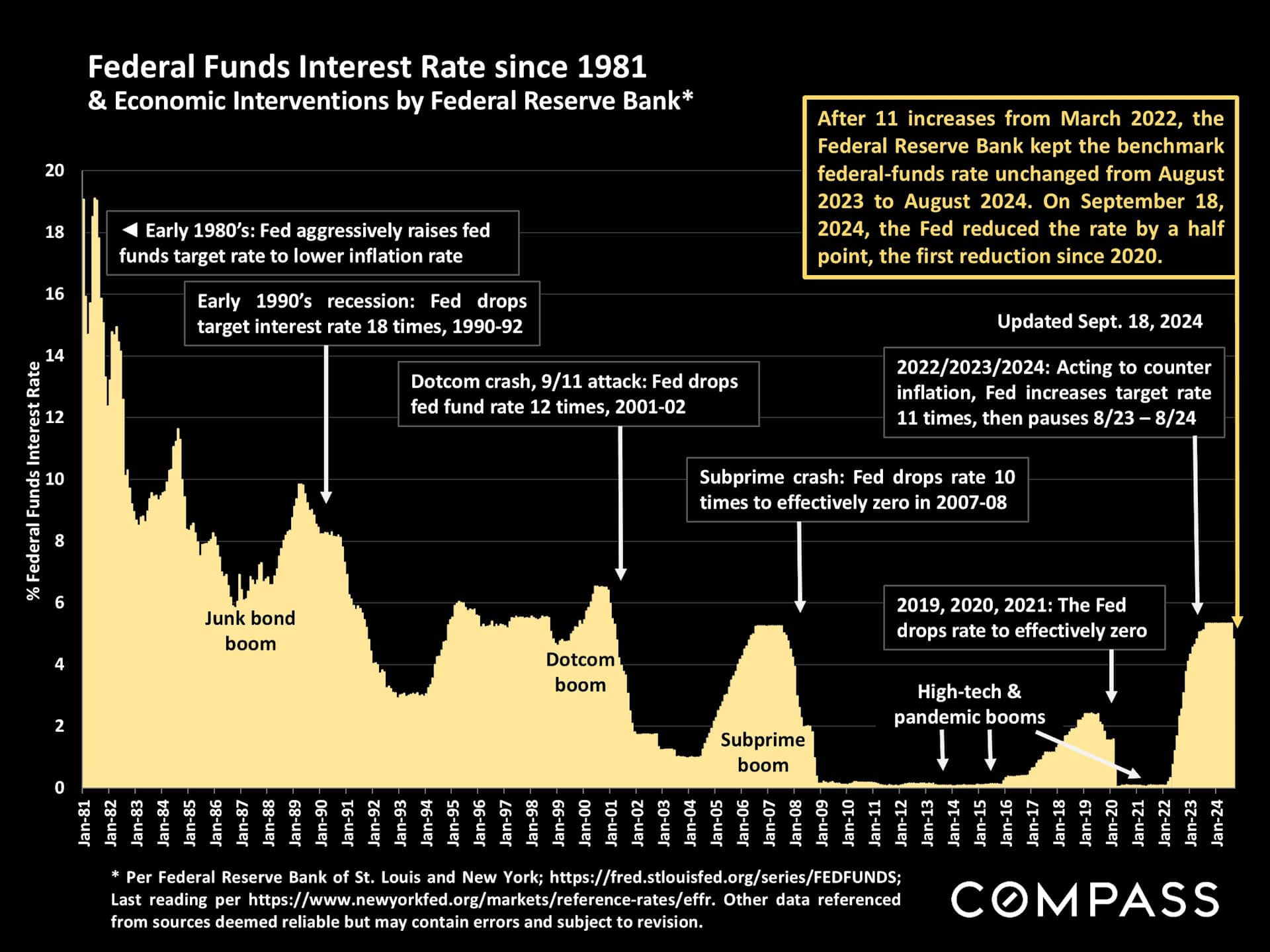

Federal Funds Rate: A Historic Perspective

This chart highlights the Federal Funds Interest Rate from 1981 to 2024, showcasing several pivotal moments. The Fed has historically used interest rate adjustments to influence inflation, economic growth, and employment levels.

- Early 1980s: The Fed aggressively raised interest rates to combat sky-high inflation, peaking at 18%.

- Early 1990s: To address the recession, the Fed dropped rates 18 times between 1990-1992.

- 2007-2008 Subprime Crash: The Fed slashed rates 10 times, bringing them effectively to zero in 2008 to stimulate economic recovery.

- 2022-2023 Rate Increases: As inflation soared, the Fed raised rates 11 times to counter rising prices. This continued until a pause in August 2023.

Now, with inflation decreasing and economic conditions stabilizing, the Fed's rate cut signals a potential pivot in monetary policy aimed at encouraging growth while avoiding a return to high inflation. For consumers and businesses, this could mean lower borrowing costs in the near term.

How the Fed's Rate Cut Affects Buying and Selling Real Estate

The recent rate cut by the Federal Reserve is a significant shift that brings both opportunities and considerations for those looking to buy or sell a home. Understanding how this affects the real estate market can help you make informed decisions and capitalize on current conditions.

For Homebuyers: Lower Borrowing Costs and Increased Affordability

One of the most immediate effects of the Fed’s rate cut is the reduction in mortgage interest rates, which have now dropped to just above 6%. This change means:

- Lower Monthly Payments: With mortgage rates falling, homebuyers can enjoy lower monthly payments, making it easier to afford more house for your money.

- Increased Purchasing Power: As interest rates drop, your purchasing power increases, allowing you to qualify for a higher loan amount. This can be a game-changer, especially in competitive markets where every bit of extra budget helps.

- Refinancing Opportunities: If you already own a home, now might be the ideal time to refinance your mortgage at a lower rate, potentially saving thousands of dollars over the life of your loan.

Pro Tip: With rates at some of their lowest levels since early 2022, this is an excellent opportunity for first-time buyers or anyone looking to upgrade. The reduced borrowing costs make it easier to enter the market or move up to your dream home. Don’t wait, as these conditions may not last!

For Sellers: Increased Buyer Demand and Market Advantage

The impact of lower interest rates isn’t just good news for buyers—it’s beneficial for sellers too. Here’s how:

- More Buyers Entering the Market: As mortgage rates drop, more buyers are likely to enter the market, increasing demand for properties. This heightened interest can lead to faster sales and potentially higher offers on your home.

- Higher Selling Prices: When more buyers are competing for available homes, sellers often have the upper hand. This increased demand can drive up property values, allowing you to sell at a premium.

- Quicker Sales: Homes tend to sell faster in a low-interest-rate environment because buyers are eager to lock in favorable rates. This could mean fewer days on the market and a smoother selling process for you.

Pro Tip: If you're considering selling, now might be the perfect time to list your property. Take advantage of the current market dynamics, where motivated buyers are actively searching for homes, and you have the potential to maximize your return on investment.

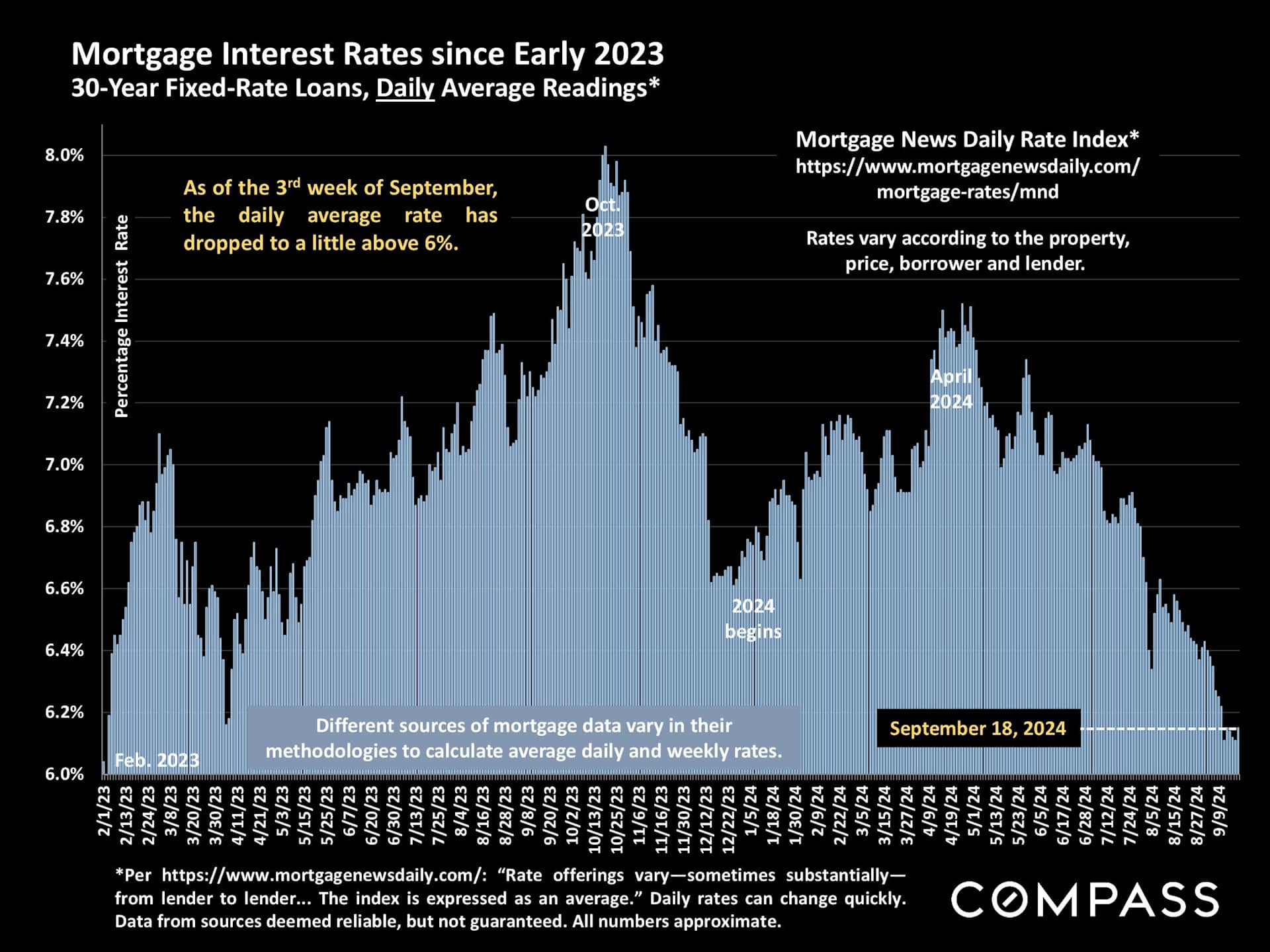

Mortgage Interest Rates: A Welcome Decline

Mortgage interest rates, closely tied to the Fed’s decisions, have also shown significant movement. In the second chart, the daily average for 30-year fixed-rate loans in 2024 has fallen from a peak of over 7.8% in late 2023 to just over 6% by mid-September 2024. This trend reflects optimism in the housing market as lower mortgage rates typically translate to more affordable home financing options for buyers.

For homeowners and potential buyers, this rate cut could open doors to refinancing opportunities or enable new buyers to secure more favorable terms.

Financial Markets: A Roller Coaster Ride

The third chart highlights the performance of the S&P 500 and Nasdaq indices from January 2023 through September 2024. Both indices have seen robust growth, with the Nasdaq reaching a nearly 70% increase by mid-July 2024, and the S&P 500 gaining over 40% in the same period.

Despite occasional volatility, particularly influenced by tech stock swings, the markets have shown resilience and consistent upward momentum. This period of growth has rewarded investors, but as we move into the remainder of 2024, investors should stay attuned to potential market corrections, especially in light of ongoing interest rate changes.

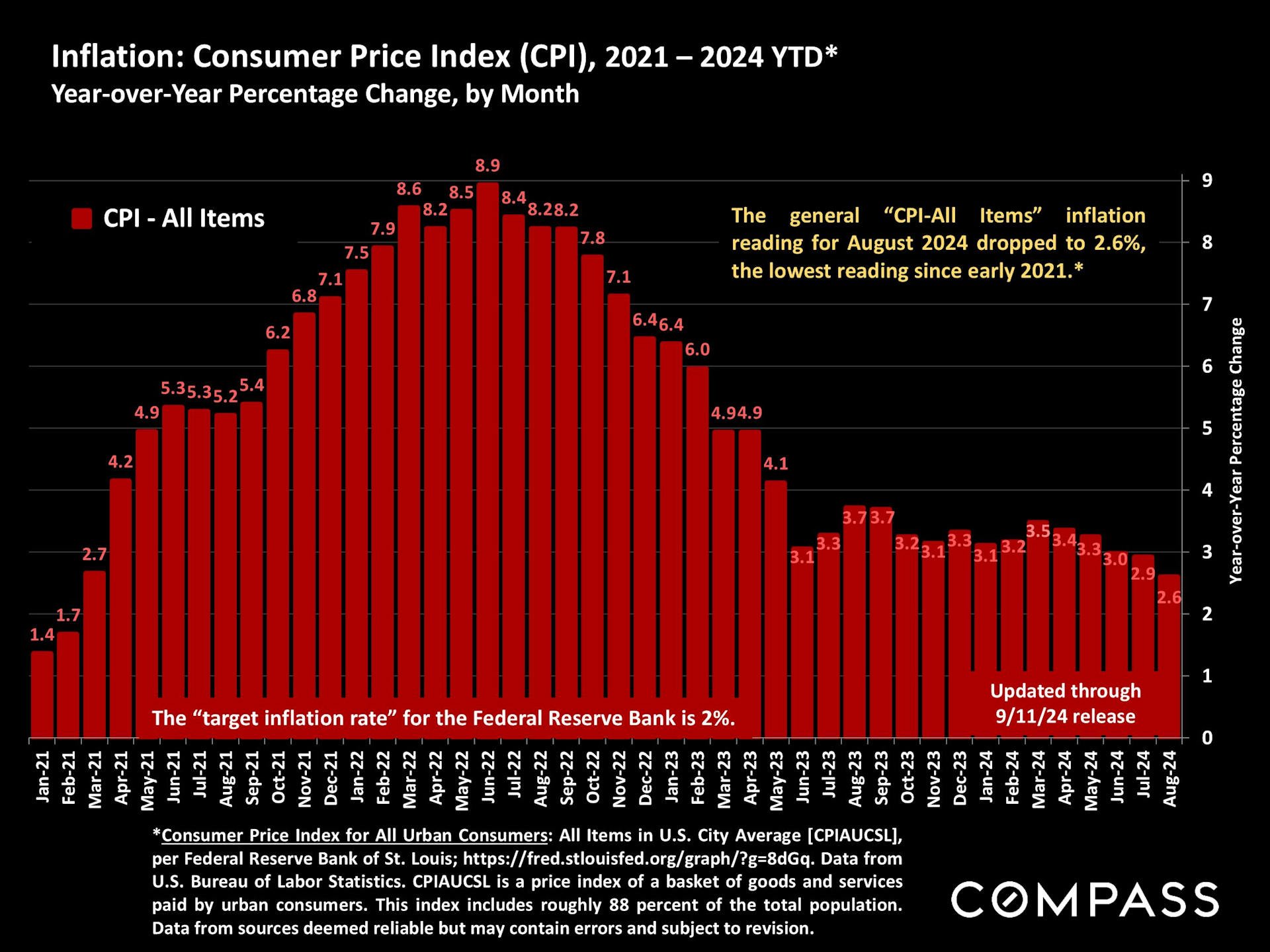

Inflation: Finally Under Control?

The last chart provides a detailed view of inflation, as measured by the Consumer Price Index (CPI), from 2021 to 2024. After peaking at 8.9% in mid-2022, inflation has steadily declined, dropping to 2.6% in August 2024, its lowest point since early 2021.

With inflation nearing the Federal Reserve’s target rate of 2%, this is a welcome relief for consumers, as price stability begins to return across goods and services. This decline in inflation has likely influenced the Fed’s decision to lower interest rates, providing further relief for borrowers and boosting consumer confidence.

What to Expect Moving Forward

As we enter the final quarter of 2024, several economic indicators point to a more stable and promising outlook:

- Interest Rates: Further reductions in the federal funds rate could ease borrowing costs, making it more affordable to finance homes, cars, and business ventures.

- Mortgage Rates: Homebuyers may experience more favorable mortgage rates, encouraging new buyers to enter the market and potentially lifting housing demand.

- Market Volatility: Investors should remain cautious as market volatility, particularly in tech stocks, may persist. However, overall market performance is expected to remain strong.

- Inflation: With inflation under control, consumers and businesses can expect more predictability in pricing, allowing for long-term financial planning.

Looking Ahead: What This Means for You

As we move into the final months of 2024, the Fed’s rate cut, lower mortgage rates, and controlled inflation open up new opportunities in the housing and financial markets. Whether you're looking to buy, sell, or refinance, the timing could be just right to take advantage of these shifts.

At Faber Real Estate Team, we specialize in guiding you through these economic changes to ensure your real estate decisions are informed and advantageous. With our deep market knowledge and commitment to providing value, we’re here to help you navigate the complexities of buying or selling a home. Reach out to us today—let’s work together to turn these market trends into your advantage.

Faber Real Estate Team | Compass

The Key to Your Dreams ®

Ben Faber DRE #01913767

[email protected]

www.faberrealestateteam.com

@faberrealestateteam

415.686.4980